Global Sourcing in Flux; Rewiring Ecommerce Supply Chains; How Hot is the Cold Chain? and other Logistics News

Logistics and supply chain news and highlights shaping the future of global logistics.

Sourcing Update: Global Trade, Regional Focus

Global sourcing is in flux. Expanding tariffs, geopolitical tensions, and trade fragmentation are forcing companies to rethink how they manage risk, balance cost, and maintain flexibility. TradeBeyond’s Q1 2026 Retail Sourcing Report shows retailers are moving away from traditional, linear supply chains and embracing regionalized, multi-hub strategies. And, rather than reacting to crises, retailers are proactively redesigning their networks by investing in digital tools and data-driven processes to anticipate disruption before it hits, the report notes.

This shift is not just about diversification; it’s about resilience. The Q1 data shows nearshoring and multi-hub sourcing are gaining traction in regions such as Mexico, Southeast Asia, and South Asia, while digital transformation allows companies to maintain end-to-end visibility across increasingly complex networks. At the same time, global growth remains steady but subdued, and cost pressures from currency fluctuations, commodity trends, and environmental regulations continue to shape sourcing decisions.

Key trends highlighted in TradeBeyond’s report include:

- Tariffs drive diversification: U.S. and retaliatory trade measures are pushing retailers to source from multiple regions to avoid overexposure.

- Regionalization on the rise: Companies are adopting nearshoring and multi-hub models to build flexible, responsive supply chains.

- Freight and cost pressures: Container rates are easing, but ongoing disruptions and regulations continue to challenge logistics.

- Digital supply chain transformation: End-to-end visibility, real-time collaboration, and data-driven decision-making are increasingly central to operations.

- Complex economics: Stabilizing commodity prices are offset by currency fluctuations and trade tensions, requiring careful cost management.

As retailers navigate this evolving landscape, the winners will be those who combine regional flexibility with digital intelligence, notes TradeBeyond. Key strategies include building supply networks that can pivot quickly, onboarding new suppliers efficiently, and maintaining visibility across the entire product lifecycle.

A separate global sourcing survey from QIMA shows some encouraging trends: after a decade of disruption, global networks are better prepared to navigate shocks and identify opportunities hidden within. Drawing on the insights of more than 1,000 businesses with international sourcing networks, The QIMA Sourcing Survey 2026 shows companies are leveraging experience to transform disruption into smarter sourcing, stronger relationships, and greater resilience in 2026.

Source: TradeBeyond

Diversification, visibility, and digitization are taking center stage, with QIMA reporting the following:

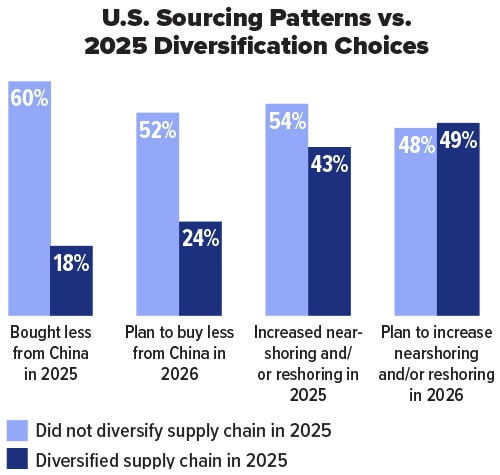

Two in five supply chains (43%) made notable sourcing geography changes in 2025 to mitigate the impact of tariffs. (See chart left)

Fully mapped networks outperform on most operational fronts, from quality to costs; 60% of respondents report supply chains that are mapped.

74% of respondents plan to invest in supply chain digitization in 2026. High digitization streamlines communication and safety compliance.

The QIMA report also notes a 2026 global sourcing outlook marked by strong U.S. optimism: only 20% of U.S. businesses expect supply chain conditions to deteriorate further in 2026.

Rewiring Ecommerce Supply Chains

Ecommerce businesses are preparing to overhaul their global supply chains as geopolitical uncertainty and disruption reshape the sector. For starters, 87% of those surveyed in new research from global 3PL Fidelity Fulfilment, in partnership with Opinion Matters, say they are likely to change their primary manufacturing locations within the next three years.

This significant restructuring of global production networks signals a new phase of supply chain strategy for the ecommerce sector, one that is focused on resilience and flexibility.

Alongside changes to manufacturing, the report—which surveyed 1,500 ecommerce businesses across the United States, UK, and Europe—shows ecommerce companies are also expanding their logistics infrastructure. Nearly nine in 10 (86%) say they are likely to open additional fulfillment centers over the next three years, reflecting a shift toward more distributed fulfillment networks. By localizing inventory closer to customers, these firms aim to reduce disruption risk, improve delivery speeds, and simplify cross-border logistics, the research shows.

Here are some additional insights from the report:

Despite ongoing economic uncertainty, confidence in supply chain resilience is rising. 88% of respondents say they are now more confident in their ability to manage supply chain shocks than they were three years ago.

Despite ongoing economic uncertainty, confidence in supply chain resilience is rising. 88% of respondents say they are now more confident in their ability to manage supply chain shocks than they were three years ago.

Commercial importance of sustainability initiatives continues to grow. 89% of ecommerce companies say their sustainability efforts have had a positive impact on their organization, rising to 93% among EU respondents, and 92% in the UK.

Commercial importance of sustainability initiatives continues to grow. 89% of ecommerce companies say their sustainability efforts have had a positive impact on their organization, rising to 93% among EU respondents, and 92% in the UK.

Ecommerce leaders prioritize customer experience (23%) ahead of both cost savings and sustainability (both 19%), underlining the continued importance of delivery performance and fulfillment quality in driving customer loyalty.

Ecommerce leaders prioritize customer experience (23%) ahead of both cost savings and sustainability (both 19%), underlining the continued importance of delivery performance and fulfillment quality in driving customer loyalty.

Pressure Hits the Road

Due to impacts from recent severe weather and supply chain volatility, pressure is mounting across the U.S. logistics sector—and fast. A recent report from Tech.co shows the industry absorbing a surge of operational strain, with its Operational Pressure Index hitting a record high of 44 in February 2026. This marks the highest number since April 2025.

Major winter storms earlier this year disrupted freight flows, strained labor availability, and created cascading impacts across transportation networks— from delayed shipments to warehouse power outages, notes the report. Not surprisingly, 30% of logistics firms surveyed by Tech.co cite unforeseen events, including severe weather, as the primary driver of increased pressure.

In response, logistics companies are shifting their focus inward, prioritizing operational resilience over expansion. Fleet maintenance has emerged as a key strategy, with a growing share of firms investing in preventative upkeep to stabilize day-to-day operations and reduce the risk of further disruption.

The report cites these top five vehicle upkeep measures currently being implemented (by popularity among U.S. logistics businesses):

1. Preventative maintenance (70%)

2. Addressing mechanical issues (52%)

3. Upgrading/replacing components (51%)

4. Ensuring safety compliance (49%)

5. Improving fuel efficiency (40%)

Additionally, the report shows fleets face more knock-on effects from unforeseen disruptions.

These include:

Vehicle upkeep expenses: Vehicle upkeep rose by 3% from January to February 2026, and has remained the top priority while harsh weather damaged trucks and forced companies to spend more on maintenance.

Labor challenges: February saw a rise in poor working conditions as drivers were subjected to harsher driving conditions and potentially longer hours due to unpredictable delays.

Higher insurance costs: A greater number of road accidents have raised insurance prices.

Uncertain Skies Ahead

The global airfreight market is once again under strain as conflict in the Middle East disrupts capacity and clouds already weak growth expectations for 2026, according to new analysis from Xeneta. Unlike previous crises—including the pandemic and Red Sea shipping disruptions—air cargo is bearing the brunt of the shock rather than serving as a fallback to ocean freight. While demand trends have softened, the larger concern is the broader economic fallout tied to rising fuel costs, inflation, and geopolitical instability, notes Xeneta.

Stronger collaboration among shippers, forwarders, and airlines is helping maintain short-term stability as the industry adapts in real time. But the disruption is spreading beyond the Middle East, affecting major global trade lanes and reshaping contract strategies, as more shippers shift toward shorter-term agreements amid uncertainty.

“Right now, the air cargo market is suffering from a supply issue—and this will be resolved. But the longer this recovery takes will determine if it becomes a much bigger demand issue,” says Niall van de Wouw, Xeneta’s chief airfreight officer.

Additional data points from Xeneta include:

- Air cargo capacity in the Middle East remains about 30% below pre-conflict levels, tightening global supply.

- Spot rates have surged, in some lanes rising 50% to 100% within weeks due to capacity shortages and fuel costs.

- Shippers are shifting toward short-term contracts, with spot market share rising to more than half of global volumes.

- Jet fuel price increases and rerouting pressures are driving rate increases across Asia-Europe and transpacific lanes.

Industry resilience will depend on the duration of the conflict and its broader economic impact, particularly on energy markets and demand, the report concludes.

Is the Cold Chain Hot—or Not?

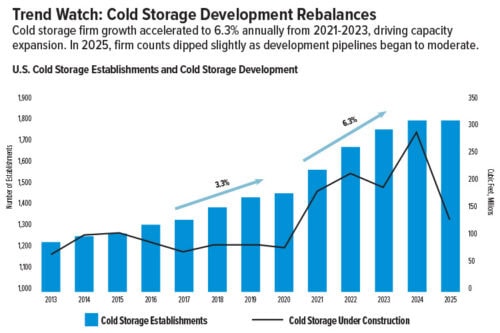

The U.S. cold storage sector is entering a reset period. After several years of aggressive development, supply has begun to outpace demand, pushing vacancy to a 20-year high even as the market recorded roughly 3.5 million square feet of positive absorption in 2025. At the same time, the development pipeline has dropped to 5.9 million square feet—the lowest level since 2020—signaling a slowdown in new construction. Softer consumer spending and elevated food prices, which rose 3.1% year over year, further weigh on near-term demand and inventory levels.

Source: Newmark

These are the key takeaways from global commercial real estate firm Newmark’s latest report, 2H 2025 U.S. Cold Storage Market Overview, which examines the sector in detail.

Beneath the surface, demand is not disappearing, it’s evolving. The report points to structural drivers such as population growth, e-grocery expansion (which posted a 32% year-over-year sales increase in Q4 2025), domestic food production, and pharmaceutical cold chain needs as continuing to support long-term growth. At the same time, occupiers are rethinking strategy in response to rising rents, which have more than doubled since 2020, prompting increased interest in ownership, automation, and operational efficiency.

Important cold chain trends outlined in Newmark’s report include:

Vacancies in transition: Elevated deliveries have pushed vacancy higher, with modern facilities at 6.1% vacancy and older assets at 7.6%, though a shrinking pipeline points to future balance.

Flight to quality accelerating: Demand is increasingly concentrated in newer facilities, while legacy space accounts for roughly 73% of total vacant square footage.

Costs reshape decisions: Rapid rent growth is driving more occupiers to explore build-to-own strategies and sale-leasebacks.

Demand drivers shift: E-grocery growth, population expansion, and pharmaceutical demand are offsetting weaker near-term food consumption, which is being pressured by inflation and slower spending.

New complexities emerging: GLP-1 drug adoption—now used by up to 18% of U.S. adults—could reduce overall food consumption while shifting demand toward protein and fresh food categories, with implications for cold storage mix.

Cybersecurity Fears Up, AI Confidence Down

Large businesses are increasingly anxious about supply chain disruption and far less confident that AI will deliver the resilience they need, according to new research from supply chain intelligence firm Zero100.

The study, which surveyed chief operating officers (COOs) from firms with more than $1 billion in value, finds that cybersecurity is the dominant business continuity concern, while expectations for AI-driven transformation remain cautious and misaligned with what their CEOs are pitching to shareholders.

The report finds that more than one-third of businesses rank a cyber incident as the biggest threat to continuity over the next year (35%), ahead of challenges including geopolitical instability (20%), trade policy shocks (16%), and labor disruption (8%).

Cyber incidents stand out not just as the top concern, but as the fastest-moving shock companies expect to face. Nearly two thirds (62%) say they can respond to a cyber incident within minutes or hours, compared with disruptions such as tariffs, which take the vast majority of businesses days or weeks to respond to (83%).

However, opinion is sharply divided among COOs on whether AI will reduce or increase cyber risk (50% say better, vs. 43% say worse), even as a majority say it will help manage supply shortages (64%) and ease skill gaps (58%).

The research also highlights a growing credibility gap between what companies tell investors and what they believe they can deliver. Fewer than one in five COOs believe a majority of their company’s AI commitments to shareholders can be delivered on time (17%).

Expectations around agentic AI are particularly restrained. Just 7% believe agentic systems will fundamentally redesign a majority of workflows within the next two years. The most common view, held by two in five COOs (43%), is that agentic AI will reshape just 11% to 25% of workflows, pointing to selective deployment rather than wholesale transformation.

Progress on agentic AI is being slowed by organizational readiness rather than technical limitations. When asked specifically about deploying agentic AI at scale, COOs rated technology infrastructure as the most prepared area (6.2 out of 10), ahead of leadership understanding (6.0), data foundations (5.8), process maturity (5.6), and workforce skills (5.5).