Cash to Cash Time: Definition, Calculation, and Ways to Improve

Managing working capital effectively is a top priority for modern supply chain and logistics professionals. A critical metric used to evaluate this efficiency is cash to cash time. This metric serves as a vital indicator of financial health and operational agility across the enterprise.

This informational article provides a comprehensive overview of the net operating cycle, also known as the cash cycle. You will learn its precise definition, how to calculate it using a standard cash conversion cycle formula, and actionable strategies to optimize it. Let us dive into how this metric influences your company’s operational efficiency.

What Is Cash to Cash Time?

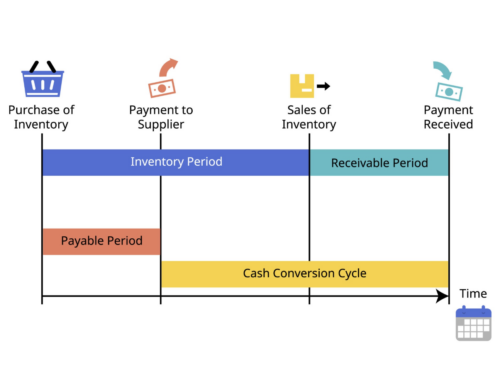

Cash to cash time represents the duration between when a business pays for raw materials and when it collects cash from customers for the finished goods sold. It tracks the flow of cash through the production and sales process. This metric is a foundational KPI for assessing a company’s cash conversion cycle.

Cash Conversion Cycle and cash flow operating cycle from purchasing inventory to cash. Source: Getty Images

Understanding this timeline helps leadership evaluate liquidity and the velocity of a company’s cash. A shorter cash conversion cycle means a business recovers its investments quickly. Conversely, a prolonged cash cycle ties up vital working capital that could otherwise fund growth initiatives.

Components of Cash to Cash Time

The overall cash to cash cycle is determined by three fundamental components of supply chain operations:

- Days Inventory Outstanding (DIO): The average time period a company takes to convert raw materials into finished products and complete the sales process.

- Days Sales Outstanding (DSO): The average number of days it takes a business to collect customer payments after a sale is finalized.

- Days Payable Outstanding (DPO): The average time a business takes to pay suppliers for its acquired inventory and materials.

Collectively, these components dictate the speed of your cash flows. Balancing days inventory, payment collection, and supplier payment terms determines how much capital remains trapped in operations.

How to Calculate Cash to Cash Time

To measure your cash cycle time, you must look at your balance sheet and income statement. The standard cash conversion cycle formula aggregates the timelines of inventory, receivables, and payables.

The mathematical equation is expressed as follows:

Cash to Cash Time = Days Inventory Outstanding + Days Sales Outstanding – Days Payable Outstanding

To perform this calculation accurately, you must first determine the individual components based on a specific time period (usually 365 days):

| Metric Component | Formula | Operational Meaning |

| Days Inventory Outstanding (DIO) | Average Inventory / Cost of Goods Sold x Days | Measures inventory management and inventory turnover velocity. |

| Days Sales Outstanding (DSO) | Average Accounts Receivable / Total Credit Sales x Days | Tracks how fast the credit department can collect payment. |

| Days Payable Outstanding (DPO) | Average Accounts Payable / Cost of Goods Sold x Days | Shows how long the company takes to pay suppliers. |

Managing these elements efficiently can lead to a negative cash conversion cycle. A negative cycle means a company collects cash from sales before it pays suppliers for the initial inventory, generating free cash flows to fund ongoing company operations.

Importance of Managing Cash to Cash Time

Effectively managing your cash to cash cycle time directly impacts corporate financial performance and organizational resilience. According to a landmark study on working capital by McKinsey & Company, maximizing operational cash flow yields a permanent competitive advantage.

Improve Liquidity

Optimizing your company’s cash conversion cycle accelerates cash velocity. This optimization ensures that more cash remains readily available on the balance sheet. Enhanced liquidity allows organizations to meet sudden obligations without disrupting the broader supply chain.

Reduce Financing Needs

When a company takes less time to collect cash, its reliance on external financing decreases. Minimizing debt service fees protects net margins. Consequently, liberated company’s cash can be reallocated directly to high-yield corporate investments.

Enhanced Response to Market Changes

An agile cash cycle time enables organizations to respond dynamically to shifting customer demand. Businesses with unburdened working capital can pivot production schedules rapidly. This agility allows them to outmaneuver rigid industry competitors during economic disruptions.

Strategies to Improve Cash to Cash Time

Shortening your cash cycle requires cross-functional collaboration between procurement, logistics, and finance teams.

- Optimize Inventory Management: Implement lean supply chain strategies, such as Just-in-Time (JIT) replenishment, to reduce days inventory. Enhancing inventory turnover ensures you do not hold excessive entire inventory, which drives up holding costs.

- Enhance Receivables Collection: Streamline the accounts receivable process by deploying automated invoicing platforms. Shorten days sales outstanding dso by offering nominal early payment discounts to encourage prompt customer payments.

- Extend Payables Period: Request extended payment terms during supplier contract negotiations. Increasing days payables outstanding allows you to utilize supplier credit longer without harming vendor relationships.

Supply Chain Insight: A good cash conversion cycle varies significantly by industry. For asset-heavy manufacturing, 45 days might be stellar, whereas ecommerce leaders often maintain a negative cycle. Benchmarking against your specific peers is vital.

Challenges in Optimizing Cash to Cash Time

Optimizing a company’s operational efficiency is rarely a straightforward task. Supply chain leaders often face systemic market conditions that disrupt cash workflows. For instance, global logistics delays can artificially inflate inventory outstanding, ruining even efficient inventory management plans.

Furthermore, aggressive tactics can backfire on company’s management. Forcing prolonged payment terms on strategic vendors can damage supply chain stability, as noted in discussions on the financialization of supply chains by Spend Matters. Striking a sustainable balance between internal financial metrics and vendor health is critical.

Conclusion

Monitoring and refining your cash to cash time is a critical requirement for sustaining modern corporate health. By comprehensively evaluating your days sales, inventory velocity, and accounts payable strategies, you can unlock significant liquidity trapped on your balance sheet.

Ultimately, organizations that master the cash to cash cycle secure the financial freedom required to invest in volatile markets. Assess your operational metrics today to optimize your cash flow, satisfy customer demand, and build a more resilient end-to-end supply chain.