5 GenAI Trends, Freight Forecast & Other Supply Chain News

Today’s top supply chain news stories.

Disruptions Keep Disrupting

If it seems like supply chain disruptions are the new norm, that’s because they have been this year. Resilinc, a supply chain resiliency solutions provider, has unveiled new data showing that the overall number of disruptions from January through June 2024 is up 30% over the same period last year.

Resilinc’s EventWatchAI platform, which monitors disruptions globally by analyzing nearly 5 billion data feeds annually, reported 10,629 supply chain disruptions in the first half of 2024. The life sciences, healthcare, general manufacturing, high-tech, and auto industries bore the brunt of the impact.

The top 10 reported disruptions in the first half of 2024 were:

1. Factory fires

2. Labor disruptions

3. Mergers & acquisitions

4. Leadership transition

5. Factory disruption

6. Business sale

7. Legal action

8. Recall

9. Extreme weather

10. Cyber attack

Key takeaways include the following:

- Major disruptions stemmed from compliance and ESG issues, labor unrest, and extreme weather events.

- Regulatory changes and ESG legislation drove year-over-year increases in fines, legal actions, and labor violations.

- Economic pressures led to surges in bankruptcies and force majeures.

- Labor disruptions rose 42% and extreme weather notifications jumped nearly 130%.

- Over half of these disruptions were severe enough to activate WarRooms on Resilinc’s platform, facilitating swift responses.

Freight Forecast: Mixed Message

Intense price competition among parcel carriers and stagnant truckload rates has yielded good news for shippers, according to the Q3 2024 TD Cowen/AFS Freight Index, released by AFS Logistics and TD Cowen. However, a favorable market for shippers isn’t the only takeaway from the Index, which provides predictive pricing for truckload, LTL, and parcel transportation markets. Here are some key highlights:

- Uneven demand and capacity imbalances in the LTL segment. LTL carriers maintain pricing discipline, while parcel carriers engage in aggressive discounting, and truckload rates have remained flat for the sixth consecutive quarter.

- After establishing a floor in Q2 2023, truckload rates are projected to remain low in Q3 2024, with a slight decline expected. Despite some upward pressure from spot market increases, contract rates continue to decrease slightly.

- Parcel carriers are caught in a cycle. They are bouncing between frequent surcharge hikes and heavy discounting to compete for limited volumes, leading to a decline in the ground parcel rate per package index. The express parcel index is also expected to fall, driven by seasonal trends and ongoing discounting.

- LTL carriers show discipline in maintaining elevated rates, despite a decrease in cost per shipment due to lighter weights and lower fuel surcharges. The LTL rate per pound index is projected to see modest growth.

- Shippers are capitalizing on cost-saving opportunities by shifting lighter freight to LTL networks and consolidating heavier freight into multi-stop truckloads.

A Deep Dive on GenAI

Rapidly evolving generative AI technology is making waves across all facets of business—and the supply chain is high on that list. Supply chain and logistics leaders are working overtime to learn to harness the power of GenAI and determine how to implement it across their organizations at speed and scale.

To gain deeper insights into GenAI’s long-term value and the risks of overemphasizing immediate outcomes such as productivity improvements, HFS Research, in partnership with Genpact, a global professional services firm, surveyed 550 senior global executives, including many in supply chain roles.

Here are five key findings:

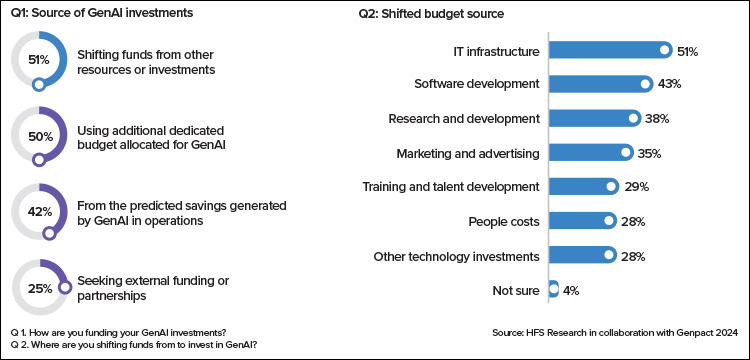

1. Most enterprises are early in their GenAI journeys but are placing big bets. Despite only 5% of enterprises having mature GenAI initiatives, a significant majority are gearing up for a technological transformation. Approximately 61% of executives are dedicating up to 10% of their tech budgets to explore and expand GenAI capabilities.

2. Executives view GenAI as a catalyst for creating new value within two years but caution against overemphasizing productivity. 74% of executives anticipate GenAI will be a springboard for value creation, driving not only productivity gains, but also customer satisfaction, revenue growth, and a competitive edge—all expected to materialize within two years. However, concerns loom as 52% caution against overemphasizing productivity, citing potential negative impacts on the employee experience.

3. Quality data is the linchpin for the successful deployment of GenAI initiatives. Organizations are challenged with several hurdles, including data quality and strategy. Notably, there’s a hesitancy around data sharing, with only 16% of enterprises using their proprietary data, underscoring the urgent need for a robust data strategy.

4. Embrace GenAI’s transformative power, but don’t lose sight of the human element. Bridging the talent divide is crucial, as 36% of executives report a scarcity of skilled professionals. Finding the balance between technical and business skills will be vital. However, in the short term, technical skills gain importance.

5. Enterprises need an ecosystem for GenAI success, but current time- and material-driven engagement models will be rendered useless in the AI era. Executives emphasize the need for a diverse ecosystem, highlighting the importance of partnerships that support talent acquisition and skill development. Additionally, 80% recognize the need to transition to performance- and purpose-driven commercial models with partners to capitalize fully on GenAI’s potential.

Investing in GenAI: Most respondents are shifting funds to GenAI from other sources, including IT infrastructure, software development, and research and development.

3 Steps for Supply Chain Viability

Supply chain and procurement leaders worried about securing business viability and addressing long-term resource constraints would do well to heed this advice: Focus on urgent, tangible issues, rather than attempting to mitigate exposure to long-term constraints directly. This approach proves to be more effective in finding solutions to actually address long-term limitations, according to new research from Gartner.

The research identifies top current resource constraints that threaten business viability and defines three key categories of action where supply chain leaders should shift their strategies:

1. Motivate action by de-prioritizing long-term constraints. Supply chain leaders should instead focus on generating action through addressing the short-term risks that stakeholders are most focused on.

2. Reprioritize long-term constraints to design solutions. By engaging with relevant internal and external stakeholders, supply chain leaders can ensure both current and future constraints are considered as part of the design process.

3. Leverage the marketplace to learn and innovate. Leading companies forge partnerships with innovators, startups, and solutions providers with a clear goal in mind. They also use pilots to identify and overcome any barriers to that goal.

Optimism All Around

Dun & Bradstreet’s Q3 2024 Global Business Optimism Insights report reveals a notable rise in optimism across all five indices for the first time since Q3 2023. Overall global business optimism and financial confidence have increased by more than 12% and 23%, respectively, despite ongoing geopolitical tensions and supply chain issues, the report shows. Central banks’ moves to ease interest rates have bolstered confidence, with businesses feeling optimistic about sales, new orders, and reduced borrowing costs.

Here are the details behind the optimism:

- The Global Business Optimism Index increased 12.3% on the back of expected growth in sales, new orders, and favorable input costs amid easing global inflation. Information tech, wholesale and retail, and textile are the most optimistic sectors.

- The Global Supply Chain Continuity Index saw a marginal improvement of 1.2% stemming from businesses adjusting to the new supply chain environment, which continues to be disturbed by geopolitical tensions, longer shipping routes and climate-related disruptions. Large business optimism deteriorated significantly while smaller businesses are more optimistic.

- The Global Business Financial Confidence Index improved 12.3% as businesses are optimistic about their operating conditions and liquidity risk. Smaller businesses are now more optimistic about cash flow management given growing expectations of falling borrowing costs.

- The Global Business Investment Confidence Index increased 23.3%, signaling a meaningful uptick in optimism for capital spending, backed by an accommodative global monetary policy. Globally, small and mid-sized businesses were more confident about the environment for merger and acquisition activity than larger businesses.

- The Global Business ESG Index increased 8% as businesses look to re-engage their sustainability initiatives. In the survey, more than one in two respondents indicated increased funding for ESG-related activities.

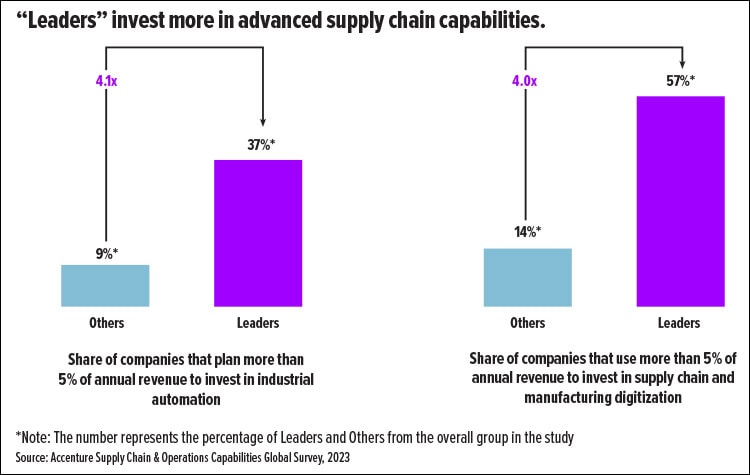

Next-Gen Tech Boosts Profitability

Looking for a way to increase profitability? Technology may hold the key. Companies with advanced supply chain capabilities enjoy 23% greater profitability compared to their peers, finds new research from Accenture. These forward-thinking companies, which are six times more likely to utilize AI and generative AI throughout their supply chains, manage to generate significant additional business value.

Accenture’s report, Next Stop, Next-Gen, identifies the top 10% of companies, referred to as “Leaders,” as achieving 23% higher profit margins and 15% better returns to shareholders between 2019 and 2023. Leaders invest heavily in sophisticated technologies, enabling them to develop and launch new products faster, create eco-friendly products, and significantly improve engineering efficiency.

Despite this, the report paints a concerning picture of overall supply chain maturity, which remains low at an average score of 36%. Companies with low supply chain maturity scores, particularly below 25%, face significant risks if they fail to evolve and adapt.

The research emphasizes that most companies still rely on outdated supply chain methods, which leaves them vulnerable in today’s dynamic economic landscape. “To remain competitive, companies must quickly adopt advanced capabilities such as real-time supplier monitoring, flexible production adjustments, and comprehensive lifecycle simulations,” says Melissa Twining-Davis, Accenture’s global operations lead for supply chains.

CrowdStrike Strikes the Supply Chain

When a CrowdStrike update in July caused a massive IT outage, crashing millions of Windows systems and disrupting air travel and other sectors, logistics professionals waited to gauge the supply chain impact.

While a fix to the CrowdStrike outage was deployed in just hours, the incident highlighted the cascading effects that technological disruptions can have on global logistics and business continuity. Two experts share their thoughts on lessons learned for the transportation and logistics sector:

“Transportation must implement multiple layers of redundancy for critical systems such as booking, scheduling, and communications platforms. Use multi-vendor solutions for clustered servers. Ensure that essential functions can continue offline or with minimal IT support, such as manual check-ins and reservations. Transportation personnel should be trained to switch to this mode if necessary. There is a need for DRP plans that include scenarios for large-scale IT failures.”

—Mike Walters, President and Co-founder, Action1

“Over-reliance on several key vendors in corporate IT highlights a broader need for supplier diversification. It goes beyond infrastructure technology into customized and high-performance components and services where single, sole, or dominant sources create consequential bottlenecks. Supplier diversification is much easier said than done, since it involves a risky and expensive process of developing a new product or service. These additional costs and risks are often dwarfed by a revenue, performance and reputational hit originating in a key supplier failure.”

—Andrei Quinn-Barabanov, Supply Chain Industry Practice Lead, Moody’s