The Invisible Shortage: How Petrochemical Shortages Could Impact Packaging

A global naphtha shortage is driving up the cost of plastic packaging across supply chains. Shippers face rising costs and new sourcing challenges as disruptions ripple from the Middle East to Asia and the U.S.

By Ashley Prince | April 21, 2026

Oil headlines have dominated the news cycle since the Strait of Hormuz effectively closed following the escalation of conflict in the Middle East in late February 2026. During that same time, however, a different crisis has been forming downstream. For shippers, the biggest threat may not be fuel costs. It may be the plastic wrapped around everything they move.

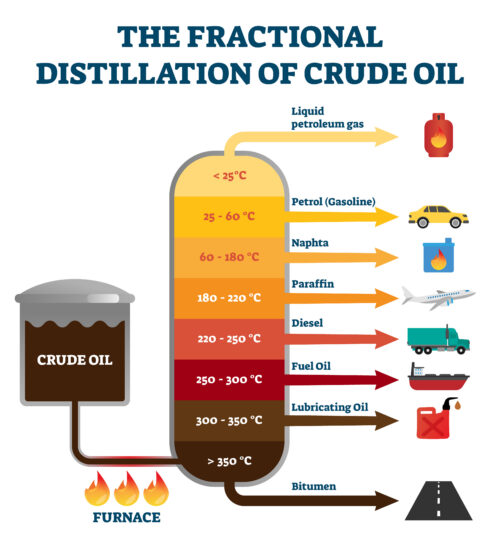

Naphtha may not be a household name, but it is an essential building block in all kinds of plastic packaging. Refineries produce it during crude oil distillation, and petrochemical plants use it as the starting point for a long chain of synthetic materials. That chain runs from naphtha through ethylene and propylene, then into polyethylene and polypropylene. Finally, it becomes the film, bags, bottles, and containers that move through virtually every supply chain.

The Middle East is the world’s dominant source of naphtha. With the Strait of Hormuz at a near standstill, that supply has been curtailed. Prices have already spiked, and the effects of production cuts are rippling outward from Asia toward every market that depends on plastic packaging to move goods.

Asia Feels the Pinch First

The impact of the naphtha shortage was felt in Asia almost immediately. As the primary petrochemical feedstock in the region, naphtha is essential for producing the building blocks used in plastics and synthetic textiles.

In mid-March, the Korea Federation of Plastics Industry Cooperatives surveyed 37 companies about the shortage. Over 70% of respondents reported receiving notices from petrochemical suppliers about potential reductions or suspensions in synthetic resin shipments. Another 92% reported being informed of price increases for raw materials.

South Korea’s largest chemical company, LG Chem, responded to the shortage quickly. The company temporarily shut down the No. 2 naphtha cracker at its Yeosu complex in March. Less than two weeks later, LG Chem made plans to import 27,000 tons of naphtha from Russia, signaling a temporary emergency supply chain restructuring.

Japanese companies are feeling similar pressure. Japan has historically relied heavily on the Middle East for its naphtha supply, and the current geopolitical situation has raised concerns about supply stability. Multiple Japanese petrochemical firms have announced production cuts, pointing to a brewing crisis that could stunt production and pressure earnings across sectors from food to technology.

The shortage has already started to affect packaging operations in Japan, according to local news sources. The price of stretch film used to secure cargo on pallets have skyrocketed, leading to supply concerns and the development of more effective stretching techniques.

The shortage has also led some Asian plastics producers to declare force majeure on supplies to customers in the Middle East. Invoking force majeure is a way for companies to be freed from contractual obligations in the event of extreme and unforeseen circumstances.

The American Impact

The United States is not insulated from the impacts of the naphtha shortage. American shale production gives domestic petrochemical manufacturers some distance from Hormuz-dependent feedstocks, but that buffer only goes so far. The Atlantic Council warns that if global petrochemical constraints persist due to upstream supply issues and overseas facility closures, consumer prices in the United States will likely rise. If China imposes export controls on certain petrochemical products, as it does for critical minerals, U.S. inflation will run higher still.

Crude oil prices and polymer prices move together. Higher crude means more expensive naphtha. More expensive naphtha means costlier ethylene and propylene. From there, the price increase works its way through PE, PP, PET, and PVC resins in sequence. By the time it reaches the packaging sector, there is nowhere left to pass it.

The IEA’s March 2026 Oil Market Report identified U.S. liquefied petroleum gas output as a key variable in managing shortages for importing countries that have lost access to Gulf feedstocks. That positions the U.S. as a potential source of relief for a strained global system. At the same time, domestic manufacturers contend with the cost pressure that comes with suddenly being in higher demand.

American shippers should not mistake geographic distance from the Strait of Hormuz for insulation. Costs are moving up across the globe. The only question is how far down the chain they will travel before someone absorbs them.

What Shippers Should Do Now

A March 2026 survey from the German Association of Plastics Processors found that 99% of packaging manufacturers were facing price increases from suppliers, though only a few were able to pass on the additional costs to their own customers. That squeeze will be felt throughout the global supply chain.

As an immediate first step, shippers across the globe should review their packaging materials exposure and make a plan to absorb higher prices. From there, companies should work to build flexibility into their sourcing operations.

Narrow and rigid procurement processes drive up costs during times of supply chain stress. When making decisions about packaging types and sourcing partners, shippers must account for the real-world costs of potential delays and shortages.

The deeper lesson from this disruption is that geopolitical risk and packaging strategy are no longer separate conversations.

Shippers that have already invested in supplier diversification, alternative material approvals, and flexible contract structures will weather this better than those that optimized purely for unit cost.