DOE Injects $17.5 Billion Into Nuclear Supply Chain to Head Off Long-Lead Bottlenecks

By Amy Roach | June 23, 2026

Building a nuclear reactor in America has historically been a high-stakes, logistical nightmare with multi-year delays and busted budgets as par for the course. Hyper-specialized components that take years just to order, let alone forge, add to the challenge.

Now, the federal government is trying a radically different approach: fixing the supply chain before the first shovel hits the dirt.

The U.S. Department of Energy (DOE) is executing a structural shift in infrastructure financing, earmarking $17.5 billion in low-interest loans specifically to shore up the front end of the nuclear power pipeline. Announced Tuesday by the DOE’s Office of Energy Dominance Financing (EDF)—formerly the Loan Programs Office—the capital injection is designed to tackle the biggest roadblock in the entire building process: the years-long wait times for the massive, specialized core parts of a reactor. By securing funding early, utilities can immediately order Tier-1 components, including the heavy steel pressure vessels that house the nuclear fuel, massive steam generators, and specialized high-power coolant pumps, long before construction begins.

The capital will be distributed across five selected projects structured as special purpose vehicles (SPVs) between utilities and technology provider Westinghouse. To qualify, each SPV must collectively contribute $1 billion in private capital into the procurement pipeline. All five projects plan to deploy the Westinghouse AP1000, the flagship U.S. pressurized water reactor.

Tackling the Long-Lead Procurement Nightmare

For logistics and procurement executives in the heavy industrial sector, the nuclear supply chain has long been a masterclass in risk. Structural components for large-scale reactors cannot be bought off the shelf; they require forging capacities that only a handful of facilities globally possess. Fragmented domestic manufacturing, coupled with strict regulations and a specialized labor deficit, frequently pushes component lead times out by multiple years.

According to EDF Director Gregory Beard, by financing the procurement of these heavy components well before breaking ground, the agency expects to compress commercial operation timelines by up to three years. The strategy aims to achieve volume-based purchasing economies, driving down the unit cost of components that usually face severe inflationary pressures during extended development cycles.

The strategy directly targets the structural failures of past projects. Southern Company’s expansion of Plant Vogtle in Georgia—which brought two AP1000 units online in 2023 and 2024—became a cautionary tale after slipping seven years behind schedule and running $17 billion over budget.

Energy Secretary Chris Wright noted that the EDF engineered this new funding framework specifically to isolate those legacy risks. A key structural difference this time around is the unbundling of technology supply from field execution. While Westinghouse remains the foundational technology supplier, the actual engineering, procurement, and construction (EPC) contracts will be awarded via a separate, competitive bidding process. Additionally, the AP1000 design is fully finalized, eliminating the rolling engineering changes that plagued Vogtle’s early supply chain logistics.

Underwritten by Hyperscale Demand

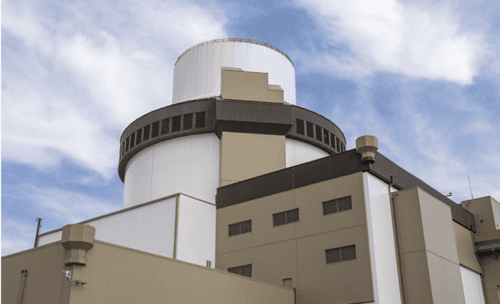

The Westinghouse AP1000 pressurized water reactor (PWR) is the most advanced commercially available nuclear power plant. Photo courtesy of Westinghouse

The administrative push to get 10 new large-scale reactors under construction by 2030 is driven by a massive, non-negotiable demand signal: the power requirements of artificial intelligence data centers.

Hyperscalers like Microsoft, Google, and Meta are scrambling to secure gigawatt-scale, carbon-free baseload power. Tech conglomerates are expected to act as the primary off-takers for these new builds through long-term power purchase agreements (PPAs), providing the revenue certainty required to underwrite the massive capital expenditures of the projects.

While the newly announced component loans are expected to stabilize the mid-tier manufacturing pipeline, the commercial operation dates for these five unselected projects are still projected for the mid-2030s.

To prevent downstream bottlenecks from choking the rollout, the administration is concurrently addressing raw material constraints. The component financing sits alongside a broader federal effort to re-establish a domestic nuclear fuel supply chain, including a recent $2.7 billion allocation for domestic uranium enrichment and ongoing negotiations to convert surplus defense plutonium stockpiles into commercial-grade fuel.

A New Playbook for Heavy Industrial Logistics?

The implications of this $17.5 billion program may extend beyond the nuclear sector. If the DOE’s pre-construction financing strategy successfully compresses project timelines and keeps budgets intact, it could establish a new federal blueprint for de-risking other massive, capital-intensive industrial supply chains.

Currently, sectors like grid-scale energy storage, deep-water offshore wind, and domestic critical mineral refining face the exact same “chicken-and-egg” procurement dilemma: developers hesitate to buy multi-million dollar components without finalized project approval, but waiting for approval pushes delivery dates out by years.

By utilizing federal capital to absorb front-end procurement risk, the government is essentially testing whether it can artificially stabilize volatile industrial supply chains. If this framework proves it can shield utilities from hyper-inflation and long-lead bottlenecks, expect to see the “procurement-first” loan model adapted for projects such as cross-country transmission lines, advanced chip manufacturing facilities, and large-scale domestic mining operations.