Ranking the Top U.S. Ports; Warehouse Taxes on the Rise; Global Trade as Election Issue; and Other News

Find out which U.S. container ports rank top for imports; see how global trade policies will impact the presidential election; and catch up on other supply chain news.

Ports Bank on Imports

For leading U.S. ports, 2023 was a surprising year in a number of ways. After a turbulent 2022 that was both boom and correction, 2023 imports defied predictions. Demand grew steadily stronger and ignored normal peak season import patterns, according to data analyzed by Descartes Datamyne. However, all was not smooth sailing for container imports.

Persistent drought lowered the level of water in the Panama Canal, slowing Asian shipments to Gulf and East Coast ports, though volumes remained strong in these regions. Maritime trade in the Red Sea came under attack, resulting in diversion away from the Suez Canal at the end of the year. And the supply chain continued a pattern of unpredictability based on fallout from the Russia/Ukraine and Hamas/Israel wars.

How did all of this impact volume at the ports? Datamyne shows a lift in import TEUs through the end of 2023, with October up 43%, November gaining 7.5%, and December improving on 2022 by 9.4%—which looks promising. Early data through March 31, 2024 (the latest available) suggests the growth has continued into the first quarter of this year, with year-over-year import volume gains of 9.4% in January, 22.3% in February, and 14.4% in March.

Here are the country’s top 15 ports ranked by 2023 import volumes measured in TEUs:

1. Los Angeles, CA

2. New York-New Jersey

3. Long Beach, CA

4. Savannah, GA

5. Houston, TX

6. Norfolk, VA

7. Charleston, SC

8. Oakland, CA

9. Tacoma, WA

10. Miami, FL

11. Baltimore, MD

12. Seattle, WA

13. Philadelphia, PA

14. Port Everglades, FL

15. Mobile, AL

Workers to Bosses: Autonomy, Please

Nobody likes an authoritarian boss—that goes for transport workers, too. A controlling and inflexible leadership style makes transport workers feel powerless and devalued, according to global research by workplace culture expert O.C. Tanner.

Findings from O.C. Tanner’s 2024 Global Culture Report reveal that 44% of transport workers have their working time strictly monitored and 39% say leaders are always watching whether or not they’re on task during work hours.

In addition, 43% of respondents say their break times are also strictly monitored, making them feel undervalued and mistrusted, with burnout and exhaustion more likely. When employees are allowed freedom in how they accomplish their work, it’s often given to a limited number of job roles or employees, the report finds.

Recommendations from the report include:

- Give every employee some level of job flexibility and influence, while recognizing the limitations of certain roles.

- Empower workers through actions such as adjusting work schedules, accommodating changing life circumstances, providing time for personal appointments, and giving workers a greater say over their workload.

“Providing all employees with some level of autonomy and flexibility at work is key, ensuring that they feel seen and valued, which in turn leads to thriving workplace cultures and better business relationships,” the report notes.

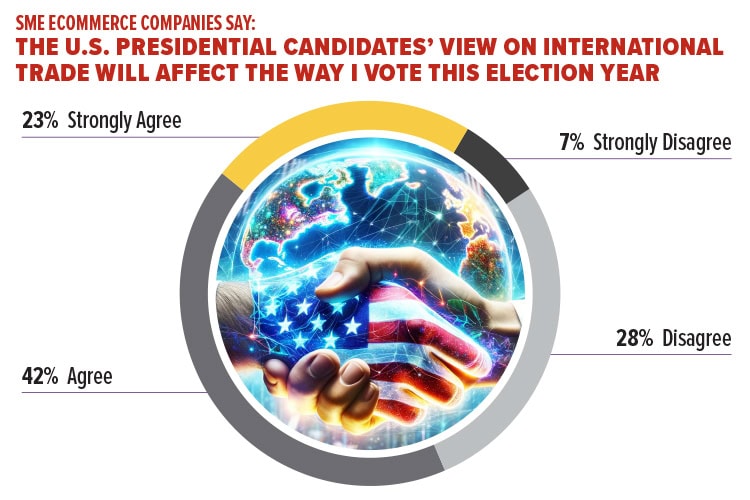

Voting for Trade Views

Source: DHL Express Survey

A subset of 23% strongly agree that these stances will significantly influence their voting decisions. This focus on trade views highlights the interconnectedness of politics and business strategies in the current economic climate.

The report, which surveyed more than 1,000 small- and mid-sized enterprises (SMEs) involved in ecommerce, also examined overall business outlook, with mostly upbeat findings. Here are some key takeaways:

- Despite economic challenges, the ecommerce business outlook is optimistic. The outlook for ecommerce sales in 2024 remains optimistic among SMEs. A significant 65% of respondents anticipate that their ecommerce sales will increase year-over-year (2023 vs. 2024), with 24% expecting a significant increase and 41% predicting a slight increase. Only 6% of respondents foresee a decrease year-over-year, indicating a strong overall confidence in the continued expansion of online sales.

- Inflation and shipping costs remain a strong concern. The survey reveals that 40% of respondents view shipping costs as the biggest threat to their business, while 38% identify inflation as their primary challenge. Likewise, 60% of respondents note that inflation is the top issue they will be following for the rest of the year, compared to other subjects like the presidential election, AI regulation, and ESG regulation.

- International business growth is a top priority for SMEs. More than half of survey respondents (53%) see international growth as the biggest opportunity for their ecommerce business. This is further supported by their priority markets for expansion, with 43% targeting the EU and UK, and 29% looking toward Mexico and Canada.

Warehouse Tax Sticker Shock

Rising taxes are the latest economic factor worrying warehouse operators and industrial developers, as tax bills for industrial buildings are experiencing significant jumps. What’s behind the sticker shock?

The increases are due to reassessments as taxing jurisdictions catch up to rising sale prices, which have surged an average of 70.4% over the past five years across 11 major U.S. and Canadian markets, notes a new whitepaper from global real estate services firm Savills.

Since property taxes are a crucial part of most municipal budgets, taxing bodies will continue aligning assessments with market values, raising the yearly levy on industrial assets. With the industrial property sector outperforming all other major asset types, more of the local property tax burden will continue to shift to warehouse occupiers.

Some key data trends highlighted in this paper include:

- Across 11 markets surveyed in the United States and Canada, property taxes have already gone up by as much as 57%.

- Over the past five years, property taxes on industrial buildings in the study markets have grown by 21.3%, primarily due to a 29.6% increase in assessments.

- Additional increases in property taxes are expected as assessments catch up to sale prices, which have grown by 70.4% compared to 4.3% for other commercial real estate sectors. For example, annual property taxes on a typical 500,000-square-foot warehouse in Northern New Jersey’s high tax market already average more than $1.1 million; this could soon increase above $1.5 million based on the analysis of recent assessments and appreciation in market value.

- The degree of under-assessment varies by market. Toronto is at the highest risk for future tax hikes, while Dallas-Fort Worth and Houston have the lowest exposure.

Spotlight: Transport Invests in IT

Source: Descartes Survey

With supply chain disruptions, changing consumer spending habits, and persistent inflation top of mind, transportation leaders are focused on improving visibility and order management and are investing more in technology. That’s the overall consensus from Descartes’ eighth annual Global Transportation Management Benchmark Survey, which is based on responses from more than 630 companies regarding their top transportation management strategies and technologies, as well as financial results and success.

Fuel costs and environmental regulations are foremost concerns in the market. Top performers continue to take aggressive actions to become more competitive and spur growth, while poorer performers are more focused on cutting costs, the report finds.

According to the survey data:

- Real-time visibility held the top spot for greatest transportation IT investment for the 7th consecutive year, followed by order management. Fleet routing climbed to the 3rd spot vs. 8th in 2023.

- 40% of shippers and logistics service providers plan to invest in transportation tech to prepare for industry and regulatory changes.

- When asked why they are investing in transport tech, cost reduction was the top reason (40%), with customer service (39%) and growth (38%) close behind. (Customer service and growth were the top choices for the past seven years.)

- 25% of respondents view transportation management systems as a “competitive weapon,” down 5% from 2023 numbers; those that view it as “not important” rose from 6% to 10%.

- The percentage of respondents who expect more than 15% growth over the next few years fell from 28% in 2023 to 12% in 2024, although overall growth expectations remain high.

- Respondents say the top three industry and regulatory changes that will have the greatest market impact over the next five years are: fuel costs (52%), environmental regulations (34%), and carrier charges (34%).

Cycle Counting: Will AI Replace Scanning?

AI-enabled vision systems may make traditional scanning-based cycle-counting processes a thing of the past. By 2027, 50% of companies with warehouse operations will leverage AI-enabled vision systems as their system of choice, according to Gartner, which made this prediction at its recent Supply Chain Symposium/Xpo in Barcelona.

“Companies are looking beyond traditional solutions as pressures mount to continuously improve operational process performance,” said Carly West, senior director analyst in the Gartner Supply Chain Practice, at the Xpo. “AI-enabled vision systems will propagate quickly in warehouse operations as the value proposition is so evident; not only for inventory management, but also monitoring that can identify safety issues and ergonomic problems for workers in real time.”

What exactly are these systems? AI-enabled vision systems are novel hyper-automation solutions that combine industrial 3D cameras, computer vision software, and advanced AI pattern-recognition technologies. These solutions leverage high-resolution vision systems combined with AI’s advanced pattern-recognition capabilities and machine learning (ML) to transform processes that, until now, have relied on manual human input.

An earlier Gartner survey (December 2023) shows that 20% of respondents have already adopted AI-enabled vision systems, and this momentum is expected to continue as the costs and performance of cameras rapidly improve.

The company also shared three recommendations for supply chain leaders who are considering deploying AI-enabled vision systems:

1. In the near term, there will not be a singular vendor or solution that fits all possible use cases. However, the value proposition of these solutions can potentially justify experimenting with multiple alternatives at low risk and low cost.

2. Start with simple processes, such as cycle counting or worker safety monitoring, that are tailor-made for an AI-enabled vision system. Leverage lessons from early initiatives to help identify additional use cases in the future.

3. Mature companies that have established good manual processes around functions such as labor management should begin to assess more advanced solutions like process ergonomic monitoring.